FAQ

Frequently asked questions and facts about purchasing your dream home!

Frequently Asked Questions

How can I determine what I house I can afford to purchase?

Determining what house you can afford to purchase involves a comprehensive assessment of your financial standing, including your income, existing debts, down payment savings, and the local housing market conditions. Key factors include getting pre-approved for a mortgage, keeping total housing costs below a certain percentage of your income, and considering all associated expenses beyond the monthly mortgage payment. Checkout our mortgage calculator to explore payment options.

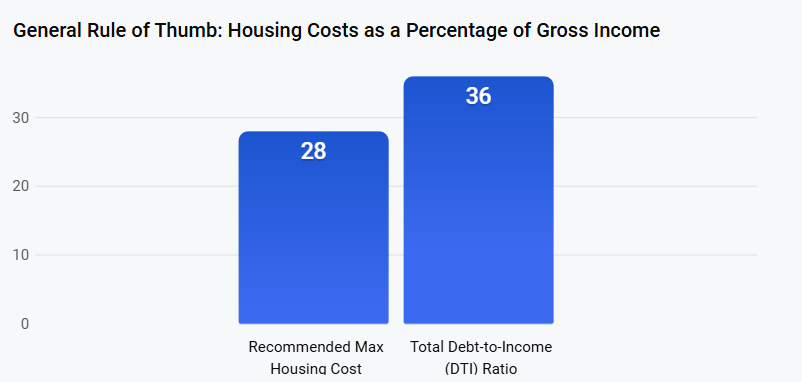

Typical Housing Costs vs. Gross Income

What Are Key Steps to Determine Affordability?

1. Assess Your Income and Savings

- Calculate Gross Income: Start by calculating your total gross monthly income (before taxes and deductions).

- Determine Your Down Payment: Factor in how much you have saved for a down payment. A down payment of at least 20% of the home’s price helps you avoid Private Mortgage Insurance (PMI), though it’s possible to put down less.

2. Evaluate Your Debt-to-Income (DTI) Ratio

Lenders use your DTI ratio to assess your ability to repay a loan. It’s calculated by dividing your total monthly debt payments by your gross monthly income.

- Front-End Ratio: This is the percentage of your gross income that goes towards housing costs (principal, interest, taxes, insurance). Many lenders prefer this to be at or below 28%.

- Back-End Ratio: This includes all your monthly debt payments (credit cards, car loans, student loans) plus your future housing costs. Lenders typically seek a total DTI ratio of 36% or less, though some programs may allow up to 43%.

3. Get Pre-Approved for a Mortgage

A mortgage pre-approval is a conditional commitment from a lender stating how much they are willing to lend you based on your financial information. This is a crucial step as it gives you a realistic budget for house hunting.

4. Factor in All Housing Expenses

Your monthly housing cost is more than just the mortgage payment (principal and interest). Be sure to include:

- Property Taxes

- Homeowner’s Insurance

- Mortgage Insurance (PMI) if your down payment is less than 20%

- Homeowner’s Association (HOA) Fees (if applicable)

- Utilities and Maintenance Costs: Budget for ongoing maintenance, repairs, and fluctuating utility bills.

5. Budget for Closing Costs

These are fees associated with completing the real estate transaction. Closing costs typically range from 2% to 5% of the total loan amount and must be paid at closing.

By carefully considering these factors and consulting with a financial advisor or mortgage lender, you can establish a clear and affordable budget for purchasing a home.

Are There Any Canadian Government Home Buying Assistance Programs?

Yes, there are several programs available to provide this assistance. Several Federal and Regional programs are listed below:

Federal Home Buying Assistance

- First Home Savings Account (FHSA): A tax-free registered plan that allows you to save up to $40,000 (with an annual contribution limit of $8,000) toward your first home.

- Home Buyers’ Plan (HBP): Allows first-time buyers to withdraw up to $60,000 tax-free from their RRSPs to put toward a home purchase.

- First-Time Home Buyer’s Tax Credit (HBTC): Provides a non-refundable tax credit of up to $1,500 (calculated as 15% of $10,000) for eligible buyers.

- Note: The federal First-Time Home Buyer Incentive (a shared equity program similar to Australia’s BuyAssist) ceased accepting applications on March 21, 2024.

Regional & Specific Programs

- Montreal Home Purchase Assistance: Offers subsidies between $5,000 and $15,000 for purchasing new homes, with potential bonuses for environmental certifications like LEED or Novoclimat.

- Manitoba Rural Homeownership: Offers forgivable loans of up to 25% of the purchase price for specific rural communities.

- New Brunswick Home Ownership: Provides repayable loans for up to 40% of an existing home’s price for those with household incomes under $40,000.

BuyAssist your next home!

BuyAssist, available on Android, iOS, and Web. Make housing affordable again.